More than ever, we should turn our trend-spotting eyes to beyond our borders. In our increasingly globalized economy, there is money to be made everywhere. Trends that used start in the United States can be seen starting in China, India, Japan, Germany, Argentina... to name but a few countries. Right now, the dollar is weak, so investing in foreign companies may make more sense now than ever.

Looking outside your borders, you will see that China is growing in leaps and bounds, which means it needs more and more water systems, but it has a serious pollution problem.

Follow the company trail, and you'll find Veolia Environnement (VE), the world's largest water utility. Veolia has four divisions: Veolia Water (water), Onyx (waste management), Dalkia (energy services) and Connex (transportation). Based in France, it has a international presence; among recent acquisitions are waste management companies in the UK, Belgium and Germany. Even more importantly, it keeps winning contracts in China for water management and purification. This January, it struck a contract to acquire 45% of the Lanzhou water supply company in the capital of the Gansu province.

Last week, it announced it won a 30-year contract to supply drinking water to Tianjin, China to supply drinking water. If Veolia keeps winning these long-term contracts in this fast-growing market, I think it is a terrific pick.

However, the potential in China comes with an asterix. While they've opened their borders and embraced the capitalist model, they still have a communist government and the rules are very different there than here in the US. This brings me to my second point about this "World is Your Oyster" trend tip. Just because something looks like a good financial opportunity abroad, doesn't mean you don't have to be extra vigilant. You must tread lightly and do your research. Authoritarian governments can interfere with the ability of foreign companies to do business in these territories.

Type of stock: The largest water utility in the world, Veolia is engaged in waste management, and related services -- a necessary business in polluted, fast-growing areas like China.

Price target: Trading at $85, this stock has gotten a boost this past week. I think the trend toward global businesses involved in environmental clean-up -- particularly in the water arena -- is hot, and I think that even at this price we'll see real growth in this stock in the next few years.

Water: The 21st Century's Oil

Is water a commodity?

It's a question that more and more investors are asking these days. The media has been full of stories about rising water scarcity: water lawsuits in the American Southwest; growing demand for water for ethanol plants; drought conditions in key grain-producing countries like Australia. Water's role in the global economy is becoming both more real, and more visible.

It’s not entirely a new idea. An article in Fortune Magazine back in May of 2000 stated, "Water promises to be to the 21st century what oil was to the 20th century: the precious commodity that determines the wealth of nations."

Really? Is water a commodity? Is it a new “hard asset,” and something that investors should include in their portfolios?

We consider the case…

Fungibility And Liquidity

To the academic community, two key hallmarks of what makes a commodity a commodity are fungibility and liquidity. Water passes both tests.

For starters, it is thoroughly fungible. Water from one source is often the same as water from another source. The price and marketing claims of Fiji Water notwithstanding, drinking water in Manhattan is about the same as drinking water in Canada, and irrigation water in California is the same as irrigation water in Ohio.

Is it liquid? We don’t mean in the obvious sense. Rather, can you exchange it for money? Increasingly, the answer to that question is yes as well. While you're not going to fill up a tanker truck and try and hawk it on Fifth Avenue, farmers are selling it (or at least the pumping rights to it) in large cities, and there is an active market for water in many communities.

s It Scarce And Necessary?

While water may meet the academic requirements of a commodity, no one would care if there wasn’t an overhang of scarcity … and a value … associated with it.

In the U.S., water still comes out of your tap clean and ready to use, for pennies a gallon; that contrasts with, say, oil, which costs a lot and is only available through targeted supplies. But like oil, demand for water is rising. Cities, companies, factories and agriculture all use a lot of it, and depend on it for function. Water is essential for life and for business, and there’s only so much of it. And increasingly, the price of water is rising.

At home, more and more cities are installing meters that measure the amount of water you use, and charge accordingly. In the past, water utilities simply applied a fixed fee tied to either your neighborhood, the size of your house or the number of bathrooms you had. But as the value of water increased, we’re increasingly being charged for that cost. (In its refined and packaged state [think plastic bottles], water can already be as expensive as heck … more expensive per gallon than gasoline.)

Abroad, the competition for water is more high-stakes. Kingdoms in the Middle East are spending huge sums of money to build desalinization plants, and farmers around the world are buying and settling water rights for large sums.

Jeff Saut said that investing in land with good access to water … like Brazil … may be a very smart move over the next few decades. As water scarcity grows, the value we attach to water will grow as well, and that will raise costs.

According to the World Resources Institute, global water consumption grew at twice the rate of the population during the 20th century. That rate continues today, as populations grow and countries like China and India put pressure on their water resources to fuel industrial growth. In sum, the long-standing rumors about water scarcity look like they may finally come true.

But Isn’t There Water Everywhere?

This pending scarcity flies in the face of our natural assumptions. We live on a planet covered in water—roughly 70% of our world is water. The problem is that 97% of that is salt water. Great for fish, not so good for humans. Of the world's fresh water, only 1% is available for drinking, with the remaining 2% trapped in glaciers and ice. "Water, water, every where, nor any drop to drink" is a well-known saying for a reason.

But isn't water itself a renewable resource? Through evaporation and precipitation, water is recycled. But just because it was potable water in the first go-round doesn't mean it will be potable water after the cycle is completed. Pollution and other factors are shrinking the supply of clean, potable water, while demand continues to grow. Increasingly, for water to be useful, it needs to be mined, processed, packaged, moved and delivered. Just like oil, coal, gas or gold.

Here's an example.

We have farmers planting corn all over the place because of the ethanol boom. Corn is a thirsty crop, requiring 118 gallons to grow 1 pound of corn. Once you have the corn, estimates vary from 3 to 15 gallons of water needed to produce 1 gallon of ethanol. (Those are just the rational estimates; you can add or subtract decimal places if you troll for statistics hard enough.)

All of that water has to come from somewhere and most often, it has to come from someone else. Cities and states have to make decisions on what is most important for their growth and development, and how that impacts their neighbors. For example, Nebraska has an agreement with Kansas over water rights because they share the same source water (the Ogallala aquifer that stretches under eight states from South Dakota to Texas).

Farmers in Nebraska are under water restrictions as to how much they can irrigate because the water level has to remain constant so that Kansas can get what was agreed to. They say good fences make good neighbors. In this day and age it may well be that good water management is the virtual fence.

Outside the developed world, the need for potable water is even greater, and making the existing water potable or transporting in potable water can be extremely challenging.

But all of these challenges can bring market opportunities.

Market Plays

Water is scarce, demand is going up (due to population increases, agricultural increases, etc.) and you want to get into the water market. What’s the play?

Since backing that tanker up to your tap is out, you'll need to look elsewhere; holding physical water is prohibitively expensive, and while there has been talk of starting a water futures market, one cryptic line on a website does not a market make; it’s not clear how such a futures market would work. One could imagine that water rights would be negotiated and sold on an exchange in the future, but we’re not there yet.

Right now, the best way to play the market is through equities, and fortunately, there are a number of indexes and ETFs that provide exposure to companies involved in the space: water utility companies, pipe and pump manufacturers, filtration and treatment companies, and water management companies. These are the companies who are directly involved in taking water to where it is needed, and as the value of water grows, the demand for these products will likely grow as well.

Currently, there are three water-focused ETFs in the United States:

• Powershares Water Resources Portfolio (PHO)

• Powershares Global Water Portfolio (PIO)

• Claymore S&P Global Water ETF (CGW)

Each provides a different spin on the water industry, and a full comparison of the three funds is available here. All three have turned in solid performance, as this index comparing one popular water index against the S&P 500 and Dow Jones Utility Index suggests.

Should You Buy Water?

Will that performance continue? That is open for debate. As attractive as the above chart is, the real-time performance record of the water indexes is too short to answer that question definitively. But water does share some interesting characteristics with commodities like oil and copper that make it worth considering, including rising demand and falling supply, and a link to the industrial boom in China, where water scarcity is becoming more and more of an issue.

The most intriguing aspect of the water-as-a-commodity angle is the idea that, like other commodities, water investments may be non-correlated with overall economic health and the broader equity market returns. For starters, demand for water is remarkably steady.

While much is used in industrial applications, farming and domestic uses account for the majority of water consumption in this country and abroad. And while industrial demand may ebb and flow, it’s not like people are going to stop using water … recession, depression or economic boom. The demand slope for water is rising on the backs of a demographic boom, set against a shrinking supply.

Will that story of non-correlation turn into non-correlated returns? That remains to be seen. But it is a story worth watching in the commodity space.

To start with, I want to say that I own the PowerShares Water Resources Portfolio ETF (PHO). In this post I will explain why I invest in water and why PHO is my security of choice. The links for all sources noted are at the bottom of this post and should provide a bit of a linkfest for those looking to do further research.

Water is, of course, a necessity. It is a fundamental need to sustain all life on this planet. The earth is 70.8% covered by water on its surface. Only about 2.5% of that is fresh water, 68.7% of which is currently in the form of ice (source: Wikipedia).

I grew up and live in New York State where I have enjoyed excellent water quality and sanitation services throughout my life for all of my daily needs. I am lucky and I do not take it for granted.

I have been researching the state of global fresh water for many years and been fascinated by many of the numbers. The need for adequate water supply is not just a concern for the future, but for this very day in many parts of the world:

- 1 billion people do not have access to safe drinking water

- 2.6 billion people lack basic sanitation

- 2.2 million people a year die from illness caused by contaminated water

- 5,000 children a day die from diarrhea

- water use will increase by about 50 percent in the next 30 years

- an estimated 4 billion people - one half of the world’s population - will live under conditions of severe water stress in 2025

(sources: OECD, UNICEF, World Bank, WHO, WWC)

Many developing countries have grown quickly in the past few years and are emerging into world powers right now.

- developing economies grew 7.3%, or more than twice the rate in high-income countries at 3.1%

- 10.7% growth in China and 9.2% growth in India played a significant role in the recent strength of developing countries, but even excluding these two, developing countries grew 5.9 percent

(As measured by 2006 GDP. Source: World Bank).

Technological advances, an inexpensive labor supply and abundant supplies of natural resources are some of the factors that have stimulated growth in these regions. As these countries have matured, the needs for basic modern amenities have grown. To provide these essential services requires better infrastructure and resource management throughout the countries. Roads and services are part of this, but the most basic ingredients for facilitating modernization are clean water and sanitation. The World Water Council suggests developing countries will need $4.5 trillion in water infrastructure investments over the next 25 years

Developing countries are only half of the story. The developed world has growing water needs as well. In the US and parts of Europe, much of the water infrastructure is old and in need of replacement and modernization. The WWF reports:

- water loss from aging water mains in London could fill up 300 Olympic-size swimming pools daily

- countries in northern Europe and on the Atlantic are suffering recurring droughts

- in Australia, the world's driest country, salinity is a major threat to agriculture

- contamination of water supplies in Japan is a very serious issue in many areas

- in large parts of the US, increasing consumption has led to a situation where the water supply can no longer meet demands

- a combination of climate change, loss of wetlands (which store a lot of freshwater), poorly laid-out water infrastructure and water resource mismanagement, is making the water crisis truly global

(source: WWF)

In Europe, according to Kaj Bärlund, then Director of the Environment and Human Settlements Division of the United Nations Economic Commission for Europe:

- in most countries of the UN-ECE region the system of pipes to supply water is in a desperate state

- pipe systems date from before World War I and they haven't been upgraded since

- on average between 40 and 60% of the water which is produced is lost before arriving at the tap

- in some cities the lost water amounts to 80% of production

- conservative estimates are that around $10 billion (US) a year in terms of clean water is wasted

- in many cities the entire water system would need to be rebuilt

(source: UN-ECE)

Low water levels and poor management right here in the US have also helped push water concerns high up on the domestic agenda. Recent attention on drought in the Southeast is one serious example right here domestically.

- Southeast drought hits crisis point (USA Today)

- Atlanta Shudders at Prospect of Empty Faucets (NY Times)

Altogether in the US:

- 54,000 community drinking water systems provide drinking water to more than 250 million Americans

- total drinking water and waste water infrastructure needs over a twenty-year period are about $1 trillion dollars

- at least 25% of the nation's pipes are in poor shape

- by 2020, that number is expected to rise to 45%

- in systems that serve more than 100,000 people, about 30% of the pipes were between 40 and 80 years old and about 10% of the pipes were more than 80 years old

- 6 billion gallons of treated water leak from water lines every day

- community water systems nationwide have an immediate need of $12.1 billion in infrastructure investment (primarily to protect against microbiological contamination)

- more than 40 percent of lakes, ponds and reservoirs in North America are impaired because of pollution

(sources: WIN, EPA, ASCE)

The Water Infrastructure Network estimates that drinking water utilities alone will need about $480 billion over the next 20 years. The EPA's estimate is lower at around $150 billion. Each organization has their own estimates and you can do further research to see their philosophical differences.

Rep. John Duncan Jr. from Tennessee and Hon. Bruce Tobey, Mayor, Gloucester, Massachusetts said this of the total US freshwater and wastewater system:

- we need to be spending an additional $23 billion a year over and above current investments (currently about $60 billion) to keep our drinking water and waterways clean and safe

- we are seeing the simultaneous expiration of the useful life of water infrastructure installed at various points in time in history (the majority of the problem lies underground in old pipes)

- populations have reached the point of having surpassed the capacity of our water and wastewater systems to handle them

(source: US House of Representatives)

When there is inadequate water present in an area, its people have only three options:

- create infrastructure to bring in new water

- find better technology and methods to treat, distribute and conserve the water they have

- move

No matter which option is selected, in the US or abroad, there is no way to escape the high cost of water, our primary requirement for survival.

The research I have done has shown me that, in the US alone, the cost of all maintenance and repairs for freshwater and sanitation needs for the next twenty years is well over $1 trillion (despite what may actually be spent). On a global scale, the cost over the next twenty years is more than $5 trillion.

If there does exist $250 billion in water related needs each year globally, this presents an opportunity for investors. Even if only half of this money were actually spent, it will be very profitable for some companies.

Over the years I have owned a few individual water utilities and infrastructure companies. I never really found one though that gave me a comprehensive investment in water. Then, in 2005, PowerShares launched the PowerShares Water Resources Portfolio ETF. This was the first concentrated fund investing in water related infrastructure, utilities and technology. I began holding this ETF soon after its inception. I have found it to be a wonderful way to get exposure to global spending trends in fresh water and sanitation needs. It is a core long term holding in my Roth IRA.

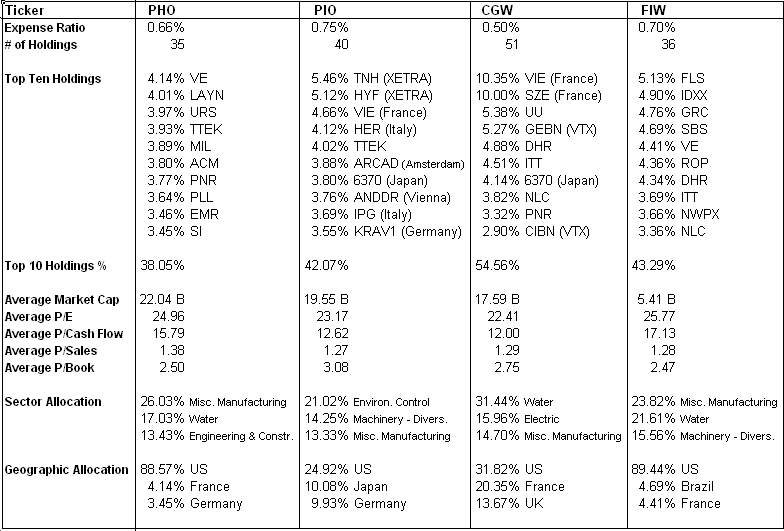

A a water ETF from Claymore (CGW) was launched in May this year. The biggest difference in the philosophy is that CGW is considered a global ETF and PHO is considered US based (it invests in US listed companies and ADRs). However, it should be noted that many of the US based companies held in PHO have sales and operations overseas and are in a prime position for global growth. When CGW came out I researched it and compared it to PHO to see if CGW may offer a better opportunity. Some articles I read around the Claymore launch seemed to suggest that CGW was the better diversified of the two.

Veolia and Suez, two French companies, comprise 20.35% of CGW's holdings as the largest positions. In fact, the top five holdings in CGW (out of 51 as of this writing) are 35.9% of the fund. The top ten holdings are 54.56% of the fund. PHO's top five and top ten holdings comprise 19.93% and 38.05% of the ETF respectively. CGW may be more diversified geographically, but certainly not in its holdings. CGW has 31.8% concentration in the US and 32.5% in France and the UK combined.

PowerShares Global Water ETF (PIO) and First Trust ISE Water (FIW) were also launched this summer (in 2007). PIO, the second water ETF from PowerShares, still has 24.92% direct exposure to US companies. There was initially a good amount of overlap between PIO and PHO. Lately, however, PowerShares has been smart and created more of a separation. This gives investors the option of augmenting PHO with PIO for a domestic and an international water ETF.

FIW is quite similar to PHO. They each invest about 89% of their assets in US companies and 4% in French based ADR's. The biggest difference in holdings is FIW's Brazilian exposure and greater holdings in the diversified machinery and metal fabrication sectors. PHO is heavier in engineering and construction. Also, FIW's top ten holdings (out of 36) comprise 43.3% of the fund.

Let us look deeper at the numbers (click to enlarge all charts):

All ETF data is according to the Bloomberg terminal on 11/23/07.

Another point I have seen mentioned a couple of times is that GE (GE) is roughly 2.99% of PHO's holdings. Some seem to think this is too high a percentage for a company where the water business accounts for 2% of sales. It should be noted though, that there are only 35 stocks held in the PHO ETF, which, if held in equal weight, would be a 2.86% position each. GE is the 17th largest holding.

I can understand the problem here for investors and for PHO management. GE is important to the global water business. You can not overlook its contribution to the industry. But how do you invest for such a small stake in the overall business? I think PHO made the right choice to include it and appreciate the fact that they have made it a lower percentage holding. Some may continue to say a 2.99% holding is too high, but in relation to a 35 stock portfolio, I think it is reasonable.

CGW, PIO and FIW are all fine ETFs. I actually like the global exposure in CGW and PIO despite the fact that I feel they are too concentrated at the top. Also, these three ETFs have existed for less than one year. CGW has assets of $315.65M, FIW of $10.49M and PIO of $241.09M.

PHO has assets of $2.14B which shows it may be the water ETF of choice among investors. I find that even though PHO is concentrated in US listed companies and ADR's, many of those companies have strong global sales. PHO holdings are also weighted far more equally than the other ETFs mentioned. Additionally I like the high concentration in engineering and construction companies. I already own PHO and I am satisfied with its performance so far. I see no reason to make a change.

Some of the stocks included in these ETFs have had a good run over the past year or so. Some have also recently corrected. The beauty of investing in a water ETF is twofold: you avoid single company risk and, through one instrument, you get coverage in utilities, infrastructure, technology and other water related industries.

This piece is solely concerned with water as a long term investment. By long term investment, I mean decades. I recommend that you thoroughly research this sector, or any sector, yourself before you put your money to work. Remember, your strategy is likely very different from mine.

Disclosure: Long PHO.