Many small pharmaceutical companies experience large percentage gains leading up to their new drug application (NDA) or potentially positive results from ongoing clinical trial results that may attract partnerships, buyouts and other attractive events for shareholders. No better company exemplifies these opportunities than Neoprobe Corporation (NEOP.OB), whose 2011 upcoming events may propel it to new 52-week highs in the blink of an eye. Here is a 20-year old biotech company with stable annual sales that cover all the overhead, two diagnostic drugs in phase 3 clinical trials about to see completion with new drug applications, and target potential sales of $3 billion and $450 million respectively. Given that the current market cap is hovering around $177 million, this would represent a significant opportunity for new and current shareholders going forward. Due to this, it is not surprising that TriPoint Global Research rated the stock (pdf) a ‘Market Outperform’ and gave it a price target of $5.00, which was quickly followed up by WBB Securities recently upgrading the stock to a target of $6.00, representing more than a 100% gain from current levels.

FDA Catalyst Companies Have Been Red Hot

Neoprobe is highly expected to gain momentum on the back of its catalysts, especially when comparing it to other companies undergoing similar circumstances:

- DepoMed (NASDAQ:DEPO) gained a whopping 143% during the last six months after Pfizer stated it would not file patent infringement lawsuit on its lead blockbuster drug, DM-1796. The company is seeking approval for the treatment of pain associated with post-herpetic neuralgia (PHN) following singles with an estimated review date of 1/30/11.

- CorCept Therapeutics (NASDAQ:CORT) appreciated 49% during the last 12 months on the back of the company’s expectations to file an NDA with the FDA by the end of the first quarter in 2011 for its lead product, CORLUX, for the treatment of Cushing’s Syndrome.

- Amarin Corporation (NASDAQ:AMRN) is by far the heavyweight winner in this category, having its share price rocket a staggering 600% during the last 12 months. These gains are primarly due to its product blockbuster lead product, AMR101 receiving highly positive clinial phase 3 results to support a potential NDA filing in 2011.

First and foremost, when analyzing Neoprobe, it is important to note that they are doing something many small cap over-the-counter companies never do — applying in order to be listed on the NYSE:AMEX major exchange. On August 3rd, the company, along with President and CEO, Mr. Bupp made this development official (pdf) and issued the following statement, “A potential listing on NYSE: AMEX would serve as a positive milestone for our Company and would enhance shareholder value. A listing would provide greater market exposure, especially to institutional investors, and provide increased liquidity for our investors.”

As of this moment, the company is well on its way to meeting the AMEX requirements, as the share price has now officially remained above the $2 mark for the last 2 weeks, as well as meeting the $50M market cap, along with the minimum $15 million market value public float and minimum of $4 million in shareholder quity. An announcement from the major exchange is expected to be announced sooner rather than later due to the fact that they have satisfied the conditions for the Standard 3 listing.

An improving financial condition also helps its cause since the Company had no outstanding debt at the end of the second quarter and had positive shareholders’ equity of $2.7 million, or $0.03 per share, versus a deficit of $9.9 million, or ($0.12) per share at the end of 2009.

Catalysts Expected During 2011

The company’s blockbuster product, Lymphoseek, a ‘first-in-class’ radiopharmaceutical designed to identify lymphatic tissue and support intra-operative biopsies during solid tumor cancer surgeries, is expected to present additional requested data from phase 3 clinical trials during first quarter 2011. This clinical trial is due to the fact that on October, 16, 2010, Neoprobe completed a pre-NDA assessment with the FDA which requested more data to support the pending NDA submission. Due to this, the company expects a potential NDA filing by mid-2011 along with a potential commercial launch.

According to a report by TriPoint Global Research (pdf), “The potential market for Lymphoseek exceeds $370 million annually, according to the Company and it will be a ‘first-in‐class’ radiopharmaceutical, making it eligible for insurance reimbursement.

Further out, there is even greater potential in the reinvigorated RIGScan CR, the original biological radio-diagnostic developed by the Company to identify occult tumor during colorectal cancer surgeries. Neoprobe is preparing a Special Protocol Assessment (SPA) for the FDA, after having received the go‐ahead from its European counterpart (the EMEA) in late 2008. A response to this SPA is expected early in 2011. Neoprobe intends to use this to help secure a partner for the further development and marketing of RIGScan CR, and a positive response to the SPA would make a licensing deal less risky and potentially more rewarding to a prospective partner.”

In addition to the initial label for lymphatic mapping in breast cancer and melanoma, there is anticipated significant off‐label use of Lymphoseek for other cancer types in the U.S., Europe and other markets, once approval for the initial indications are received and distribution is established.

Neoprobe intends to continue expanding the label for Lymphoseek to include colorectal, prostrate and other solid-tumor cancers. Also, Neoprobe has conducted early clinical work involving Lymphoseek in prior-day

injection imaging and intraoperative detection in breast cancer patients. Success in this direction would likely result in more rapid sales uptake, since hospitals would then have the opportunity to access additional

insurance reimbursement codes.

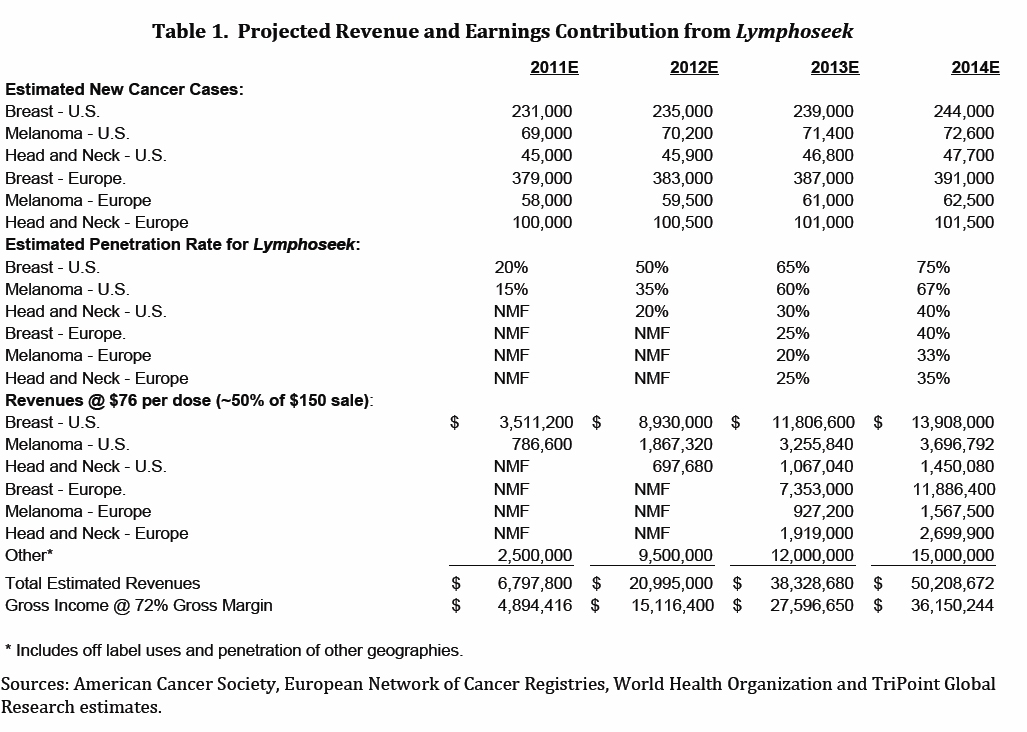

Revenue Projections

According to many analysts, the revenues going forward for the company are expected to jump drastically on the years going forward should Lymphoseek gain marketing approval. Within the first year alone, Neoprobe is projected to go from $2.3 million in revenues as per their last quarterly filling, to well over $6.8 million according to analysts (pdf). During subsequent years, revenues are expected to triple in 2012 to $20 million, then jump to $38 million in 2013 and finally top out around $50 million in 2014, as they begin to dominate market share.

(click image to enlarge)

Furthermore, Neoprobe is believed to be the market leader in gamma detection devices, with an estimated 70% market share. The total market for these systems is estimated to be in the $250 million area, with annual gross demand estimated at $20-$25 million including partner share, according to the Company. Demand is expected to accelerate if and when Lymphoseek is approved, since it would be the first radiopharmaceutical to have a label for lymphatic mapping, making it reimbursable under healthcare insurance.

1/11/11 OneMedForum Presentation Highlights

(press release found here)

- Lymphoseek Breast & Melanoma superiority trial completion expected early February, so we have to wait several more weeks for that

- Top line data to support NDA to be announced shortly afterward in early February

- 500 Lymphoseek patients with no adverse safety events are reported

- Lymphoseek gross margin now 75% (number is slightly better than was expected)

- As part of the RIGS reactivation they will be seeking the 12-year exclusive under the Biologics Price Competition and Innovation Act of 2009

- Completion of Head & Neck Sentinel trial in Q4-2011.

- 2011 sales are expected to break the $10 million level, marking a 5x increase year-over-year

During the 2008 stock market crash Neoprobe did much better than the markets, gaining 98% as a result of progress in the development of two different diagnostic agents, Lymphoseek and RIGScan CR. Suceeding these gains, in 2009 the company went on to jump 114%, followed by a 69% share appreciation in 2010 all the while avoiding the infamous flash crash.

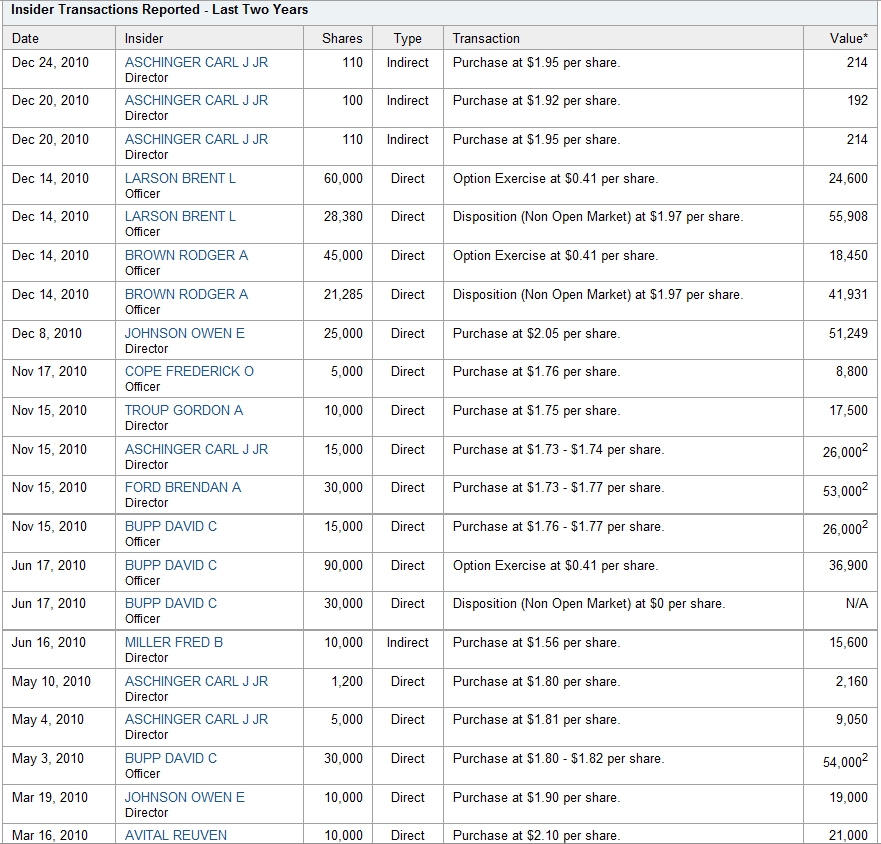

Consistent Insider Buying

Stock market veterans know very well that one of the prime metrics used in formulating opinions on a company is the insider buying. When a company’s own management team believes in its product and begins to invest in the company, it is generally believed that a favourable and optimistic future outlook is in the works. A total of 411,185 shares were purchased during 2010 by insiders, increasing their stake to 13% owned.

(click image to enlarge)

Due to all these reasons and more, it is no surprise that CNBC has also given exposure to Neoprobe by Uri Landesman, manager of the $550 million dollar Platinum Partners fund. “We expect approvals in Neoprobe’s products along with its oncology tracking drug, which will be the source of a bidding war between their distributor Cardinal and Cardinal’s competitor, Covidien”. The analyst outlines that there are many important near term milestones for its oncology products, as well as expectations of a first quarter 2011 filing for their lead compound, a first in class diagnostic for surgeons performing solid tumor procedures.

This clip can be accessed by visiting the CNBC website here.

Technical Analysis

The technical standpoint on Neoprobe shows an ‘Ascending Triangle’ pattern formation on the cusp of a breakout which could potentially appreciate the stock to a target price of $2.75. The ‘Golden Cross’ has also occurred giving further momentum to the bulls as the 50-days moving average crossed above the 200-days moving average.

This is further backed by a bullish MACD divergence and full stochastic cross which took part on low volume accumulation, generally seen just prior to a high volume breakout. Relative Strength Index (RSI) also shows a three month long uptrend that indicates continued buying pressure.

(click image to enlarge)